Americans battling the crippling cost of living crisis are fleeing to the South to more affordable states where there are favorable tax rates.

Tens and thousands of people are moving across the country to escape higher expenses which have put the squeeze on residents to areas with lower overall costs.

Florida is the most popular state people are relocating to with 16,259 looking to make the move this year, according to data from ConsumerAffairs.

While eight of the 10 states with the largest influx of new residents are in the south due to their cheaper cost of living and lower tax rates.

California is the state with the most people moving out this year with 17,824 followed by New York with 5,997 and Washington with 5,004.

Americans battling the crippling cost of living crisis are fleeing to the South to more affordable states where there are favorable tax rates

Florida remains the most popular state to move to as it boasts a better quality of life, lower cost of living and has no income taxes.

The Sunshine State does not tax earned income or investment income which attracts those looking for financial advantages.

Texas is the second most popular relocation destination with 10,602 people looking to live there this year.

Its thriving economy, strong job market, affordable cost of living and good weather makes it an attractive place to live.

The state gained over nine million residents between 2000 and 2022, according to census data.

More than 160 companies including Tesla, AT&T and Toyota have relocated to Texas in the last three years to make the most of a combination of unique competitive business advantages.

It also has no state income tax and simplifies taxes for businesses which helps them increase profits.

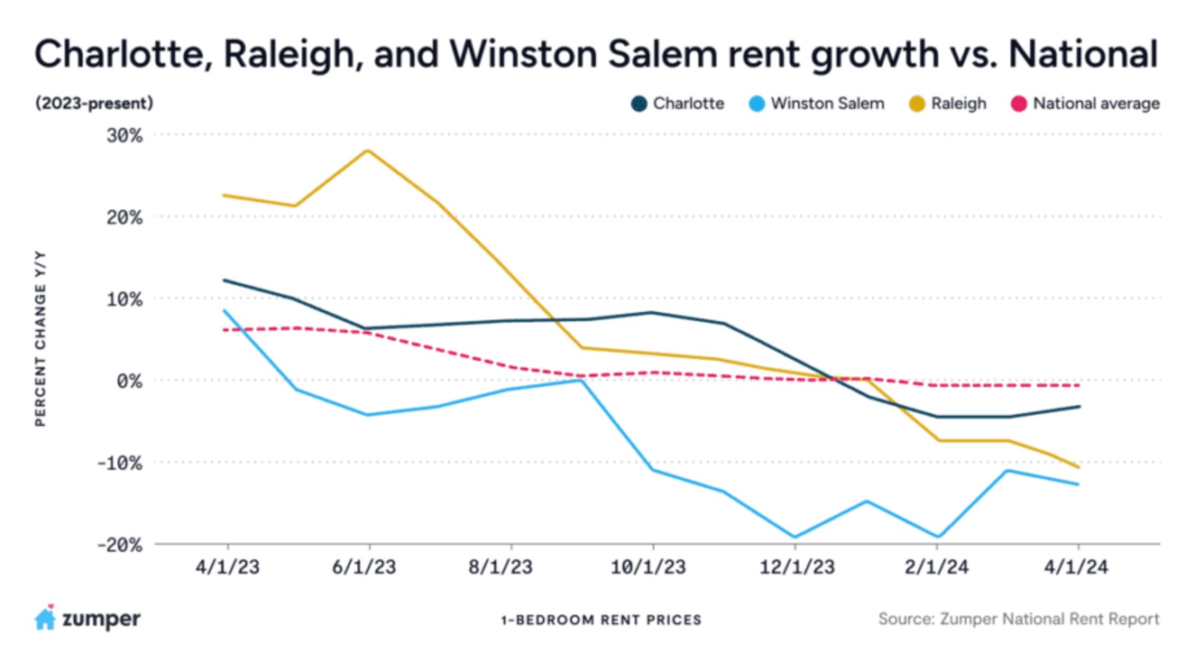

North Carolina is third on the list of states people are moving to this year with 7,970 people contemplating the move.

The state’s lower cost of living and housing is attractive to Americans priced out of other markets and it is one of the most affordable places in the country.

It boasts a strong economy and has low tax rates which attracts both individuals and businesses.

The state offers scenic views and easy access to the outdoors as well as a mild climate which provides enjoyable weather all year round.

Wilmington in North Carolina had the highest amount of people moving in last year.

Arizona and South Carolina also make up the top five states Americans are flocking to with 5,614 and 5,585 considering the move this year.

Arizona has been increasing in popularity in recent years with more and more retirees moving to the state.

The cost of living is lower than most areas with cheaper housing, utilities and taxes compared to nearby California.

It has no estate or inheritance taxes which are popular policies among elderly Americans.

An increasing number of people are moving to South Carolina to take advantage of its lower cost of living which is six percent lower than the national average.

It has lower housing, transportation and healthcare costs compared to other states.

South Carolina also boasts a comfortable climate and easy access to outdoor activities as it is close to the Atlantic ocean and blue ridge mountains.

California is the state people are leaving the most as almost 18,000 residents signified their intention to leave this year.

They are leaving the Golden State in droves, citing the high cost of living and poor quality of life as driving factors.

People have also citied politics, safety concerns and traffic as their reasons for leaving the state.

The mass exodus began in 2019 and California’s state population only rose again for the first time last year by 0.17 percent.

New York was second on the list of US states seeing the most residents leave with 5,997.

Its population has been declining in recent years with over 100,000 people leaving between July 2022 and July 2023.

The state has some of the highest costs of living in the country and many are priced out of housing.

Residents are put off by New York’s high taxes while others are choosing to leave due to crime, safety concerns and wanting a slower pace of life.

Washington came in third as 5,000 people signaled their intention to leave the state this year.

High cost of living, unaffordable housing and public safety are some of the reasons why people are fleeing.

More than 250,000 people moved out of Washington state between 2021 and 2022, according to census data. Inconvenient traffic and miserable weather are other reasons why people are looking to move out.

Colorado and Illinois rounded up the top five states which are seeing the most people move out this year.

People in Colorado have stated that they are looking for more affordable housing, lower taxes and all round higher quality of life.

They also pointed to the high cost of living as well as high levels of crime and homelessness as their reasons for leaving.

While Illinois has seen a population decline for 10 consecutive years as people continue to move out in their droves.

Residents have complained about taxes, housing and crime in the state while others mainly cited better job opportunities or retirement as their reason for leaving.